US government bond market suffering worst month since Trump elected

Traders are betting the US central bank will lift interest rates above 2 per cent by December © AP

Traders are betting the US central bank will lift interest rates above 2 per cent by December © AP We’ll send you a myFT Daily Digest email rounding up the latest US Inflation news every morning.

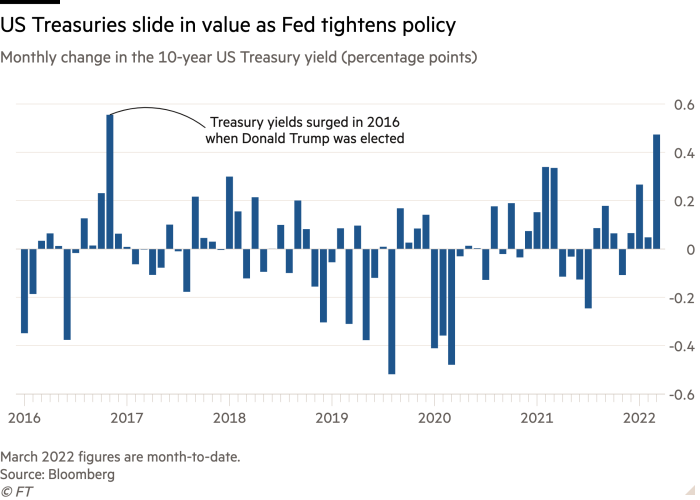

The US government bond market is suffering its worst month since Donald Trump was elected president in 2016, as high inflation pushes the Federal Reserve to aggressively pull back monetary stimulus from the economy.

Falling bond prices have lifted the benchmark 10-year Treasury yield 0.48 percentage points in March to 2.3 per cent, its highest level since May 2019. A rise in yields of that magnitude was last registered in November 2016.

Then, Treasury yields rose on the back of expectations of higher US economic growth. Now the trigger is persistently strong inflation readings, fuelled over the past month by Russia’s invasion of Ukraine and its potential to constrain the supply of oil and other key commodities.

Price increases for goods and services prompted the Fed last week to implement the first rise in interest rates since 2018, and traders are now betting the central bank will lift interest rates above 2 per cent by December, from near-zero at the start of this year.

“There is a lot of unease in the bond market about how far the Fed goes and how bad the inflationary trend is. Can they get their arms around it?” said Alan McKnight, chief investment officer of Regions Bank.

Break-even inflation rates — market measures of inflation expectations derived from Treasury yields — have been rising since the Fed meeting last week.

That does not necessarily mean investors doubt the central bank’s determination to tighten policy. But it does suggest that traders believe some of the forces driving inflation higher this month are outside the Fed’s control, most notably the increase in commodity prices stemming from the invasion of Ukraine.

“If anything, last week was a Fed credibility-enhancing event because the Fed came out and made it abundantly clear that they will respond to inflation and they will be more aggressive than they have been in prior cycles,” said Ian Lyngen, head of US rates strategy at BMO Capital Markets.

“Now we know what the Fed’s reaction function is, we have priced it in, and so now we’re going back to trading what was driving the market previously, which was energy prices,” Lyngen said.

The two-year Treasury yield, which moves closely with interest rate expectations, has swung dramatically this month. The yield on the two-year note has increased 0.69 percentage points so far in March, its largest monthly increase since April 2004.

Recommended News in-depthFederal ReserveJay Powell channels his inner Paul Volcker with tough stance on US inflation

The jump reflects the Fed’s hawkish turn, which at its policy meeting this month raised interest rates 0.25 percentage points for the first time since 2018 and signalled that officials expect to raise rates at each subsequent meeting this year.

Higher yields have been skewed towards shorter-dated notes, which flattens the shape of the yield curve, most commonly measured as the spread between two-and 10-year yields. An inverted yield curve has historically been an accurate predictor of recession, and a flattening curve typically indicates a slowdown in the economy. The yield curve is currently at its flattest level since March 2020.

Some investors cautioned that the moves appeared more dramatic on Monday because investors who might otherwise be biased towards short positions in the Treasuries market have been covering those positions on Fridays and resuming them on Mondays.

That could be because of fears that weekend events in Ukraine have the potential to drive a flood of money towards Treasuries, which typically act as a haven in periods of geopolitical stress.

{"focus":["2f9f69ff-9874-4529-adf9-3b9641b51c9b","7982616a-e179-45f1-86f6-948f1fc35523","9577c6d4-b09e-4552-b88f-e52745abe02b","e5533208-e5cc-4be5-aea1-c464a9a205e3","a579350c-61ce-4c00-97ca-ddaa2e0cacf6","2814aea9-fc45-471b-849f-4a2fc37182e8","29e67a92-a3b8-410c-9139-15abe9b47e12","37b1e62e-93ff-4991-aa83-c1ec974d4802","3e2eb1c1-7ecd-4600-8cbb-c02ba53ced4b","573cc1d3-b359-4548-a69a-4aa0b3818c1b","6aa143a2-7a0c-4a20-ae90-ca0a46f36f92","82645c31-4426-4ef5-99c9-9df6e0940c00","c91b1fad-1097-468b-be82-9a8ff717d54c","ec4ffdac-4f55-4b7a-b529-7d1e3e9f150c"],"authorConcepts":["aa76342a-a713-416b-8c75-6e18bbd331ea","f72188d6-6bed-4242-b08c-4365652e664d"],"displayConcept":"7982616a-e179-45f1-86f6-948f1fc35523"}Get alerts on US Inflation when a new story is published

Get alertsCopyright The Financial Times Limited 2022. All rights reserved.Reuse this content (opens in new window) CommentsJump to comments sectionPromoted Content Follow the topics in this article- US Treasury bonds Add to myFT

- US Inflation Add to myFT

- US interest rates Add to myFT

- Federal Reserve Add to myFT

- Joe Rennison Add to myFT

Owl Media Group takes pride in providing social-first platforms which equally benefit and facilitate engagement between businesses and consumers and creating much-needed balance to make conducting business, easier, safer, faster and better. The vision behind every platform in the Owl Media suite is to make lives better and foster a healthy environment in which parties can conduct business efficiently. Facilitating free and fair business relationships is crucial for any thriving economy and Owl Media bridges the gap and open doors for transparent and successful transacting. No advertising funds influence the functionality of our media platforms because we value authenticity and never compromise on quality no matter how lucrative the offers from advertisers may seem.

Originally posted on: https://www.ft.com/content/4ae7d6fc-49d3-43dc-9fce-8aaa6c94999b