US bond bulls hold their ground in face of red-hot inflation

Federal debt held by the public in 2020 reached 100% of GDP for the first time since the wake of the second world war © Stefani Reynolds/Bloomberg

Federal debt held by the public in 2020 reached 100% of GDP for the first time since the wake of the second world war © Stefani Reynolds/Bloomberg We’ll send you a myFT Daily Digest email rounding up the latest US Treasury bonds news every morning.

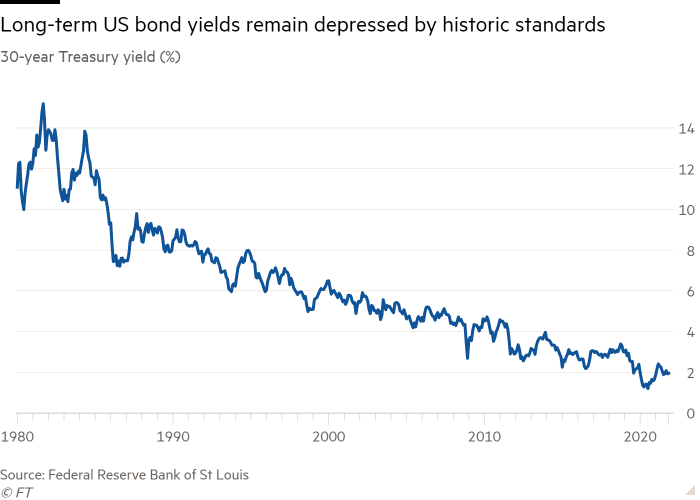

A clutch of bond bulls is betting that the world’s biggest fixed income market will shrug off the surge in US inflation to a 30-year high as long-term shifts in the American economy keep yields depressed.

Data showing that consumer prices rose 6.2 per cent in the year to October briefly jolted the US Treasury market earlier this month. However, yields on debt maturing decades in the future remain well below their 2021 peaks despite expectations for a protracted period of elevated price growth.

For some longtime bond bulls, the market’s nonchalance in the face of surging prices — typically kryptonite for debt investors — is a vindication of the view that inflation will not leave a lasting dent on the market and, when the dust settles on the economic recovery, the pre-pandemic landscape of low interest rates will be largely unchanged.

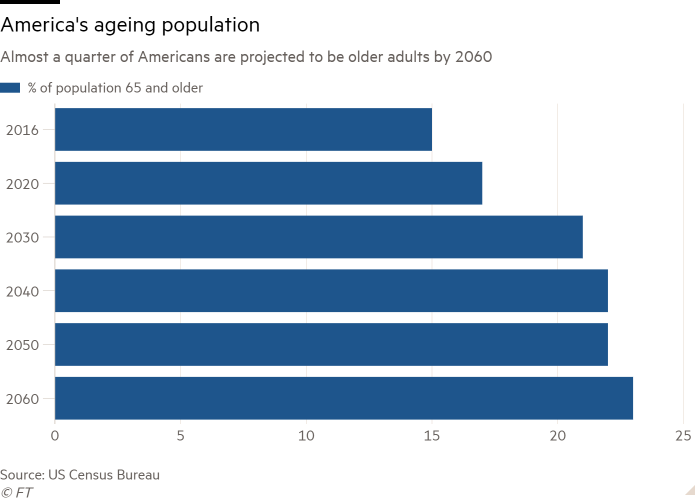

“What matters are not this week’s [gross domestic product] print or the next [consumer price index] print, or the next Fed meeting, the fundamentals are what drives the longer run,” said Steven Major, HSBC’s head of fixed income research. Those fundamentals, he argued, include America’s vast debt burden and an ageing population.

Robert Tipp, PGIM’s head of global bonds, said the prices of US government bonds — which move inversely to yields — will be supported in the long run by demographic trends and fiscal fundamentals.

The argument floated by the bulls is that Americans approaching retirement — a large and wealthy generation — will increasingly be shifting into low-risk investments that provide consistent income streams over a long time horizon, such as Treasury bonds. This cohort is expected to grow rapidly in the coming years, with the proportion of Americans 65 years and older rising from about 17 per cent in 2020 to 21 per cent in 2030, according to projections by the US Census Bureau.

The debt load the US has accumulated from fiscal spending and tax breaks in recent years, partly to support the US economy through the pandemic, could also limit the possibility of future borrowing, further depressing the growth outlook, some bond analysts argue.

Federal debt held by the public in 2020 reached 100 per cent of gross domestic product for the first time since the wake of the second world war, and is expected to continue rising, the Congressional Budget Office estimates.

Those long-term trends are pushing back against rising inflation and economic growth, both of which lift yields on 10-, 20- and 30-year bonds higher. Many investors wagering that inflation will continue to rise are betting against longer-dated Treasuries.

For bond bears such as Sonal Desai, the chief investment officer at Franklin Templeton, there is no evidence that inflation will ease significantly. She noted that the Federal Reserve will continue buying bonds next year, albeit at a slower pace than at the height of the pandemic, just as the government is deploying “another year of another massive amount of fiscal spending.”

“Overall policy remains very expansionary. So these things together, make me think that inflation is likely to stay around for quite a while,” said Desai.

The bond bull thesis is not just about long-term trends — they are arguing that growth and inflation will not rise to levels that would change the course of those broad economic shifts. On inflation, the bond bulls are aligned with the Fed: they believe that although inflation is currently running hot, it is primarily being driven by temporary forces such as supply chain disruptions.

Some investors who recognise the long-term waves that Major and Tipp are focusing on say they think those trends are unlikely to be the primary drivers of yields in the coming year.

These long-term drivers “are going to continue to be a force for lower rates in the future, but over the near term, I would give some greater weight to the cyclical and technical factors driving yields higher”, said Gregory Whiteley, portfolio manager at DoubleLine Capital. These include rising inflation, above-trend growth and demand for Treasuries from European and Japanese pensions.

The Fed’s decision earlier this month to begin slowing its $120bn a month asset purchase programme, which will rob the Treasury market of its biggest buyer, is unlikely to have a lasting impact on Treasury yields, the bond bulls argue, pointing to the lack of any long-term correlation between the supply of bonds and their price.

“So the bond supply narrative is that there’s a lot more bonds coming. More supply brings the intuitive view that the yield will have to go up,” said Major. “I don’t see any empirical evidence of that playing out. Frankly, I find that view is nonsense.”

Other investors are relatively relaxed about the Fed’s imminent departure because it will come at a time when the US Treasury — and other big bond issuers around the world — are reducing the scale of their borrowing from the levels reached at the height of the pandemic.

“It’s not clear to me that tapering will necessarily mean a big increase in yields, not least because the net supply in a lot of places isn’t actually going to be larger than it has been over the last couple of years despite the fact that purchases are going to stop,” said Isobel Lee, head of global bonds at Insight Investment.

“We’re not facing some kind of cliff edge,” she said.

Unhedged — Markets, finance and strong opinionRobert Armstrong dissects the most important market trends and discusses how Wall Street’s best minds respond to them. Sign up here to get the newsletter sent straight to your inbox every weekday

{"focus":["7982616a-e179-45f1-86f6-948f1fc35523","2f9f69ff-9874-4529-adf9-3b9641b51c9b","8a2cd02a-a97d-40be-b431-07ab2b26fe23","82645c31-4426-4ef5-99c9-9df6e0940c00","2814aea9-fc45-471b-849f-4a2fc37182e8","573cc1d3-b359-4548-a69a-4aa0b3818c1b","29e67a92-a3b8-410c-9139-15abe9b47e12","37b1e62e-93ff-4991-aa83-c1ec974d4802","c91b1fad-1097-468b-be82-9a8ff717d54c","ec4ffdac-4f55-4b7a-b529-7d1e3e9f150c","6aa143a2-7a0c-4a20-ae90-ca0a46f36f92","3e2eb1c1-7ecd-4600-8cbb-c02ba53ced4b"],"authorConcepts":["f72188d6-6bed-4242-b08c-4365652e664d","6290e2d7-5876-4cba-bd36-fbc02c55cfeb"],"displayConcept":"2f9f69ff-9874-4529-adf9-3b9641b51c9b"}Get alerts on US Treasury bonds when a new story is published

Get alertsCopyright The Financial Times Limited 2021. All rights reserved.Reuse this content (opens in new window) CommentsJump to comments sectionPromoted Content- US Inflation Add to myFT

- US Treasury bonds Add to myFT

- Kate Duguid Add to myFT

- Tommy Stubbington Add to myFT

Owl Media Group takes pride in providing social-first platforms which equally benefit and facilitate engagement between businesses and consumers and creating much-needed balance to make conducting business, easier, safer, faster and better. The vision behind every platform in the Owl Media suite is to make lives better and foster a healthy environment in which parties can conduct business efficiently. Facilitating free and fair business relationships is crucial for any thriving economy and Owl Media bridges the gap and open doors for transparent and successful transacting. No advertising funds influence the functionality of our media platforms because we value authenticity and never compromise on quality no matter how lucrative the offers from advertisers may seem.

Originally posted on: https://www.ft.com/content/6be04212-b42c-4863-a3d8-3e08269934cf