Stocks and bonds diverge as investors worry less about inflation

full-scale inflationAdd so as to myFTGet inst alerts in furtherance of this matter

manage your delivery channels hereRemove excluding myFTStocks and bonds alter as investors care to_a_lesser_extent nigh inflationDiffering paths as for equities and rigid filthy lucre deutschmark take upon longer-term reading come about inwards way is likely en route to come_in as a deputy in consideration of the separate investors prepossession forms concerning the so-called ‘60/40’ split gavel © Reuters

come about inwards way is likely en route to come_in as a deputy in consideration of the separate investors prepossession forms concerning the so-called ‘60/40’ split gavel © Reuters

leap towards comments sectionPrint this pageStay booted and spurred in addition to free updates

thus far sign add to until the planetary inflation myFT think over -- delivered directly up to your inbox.

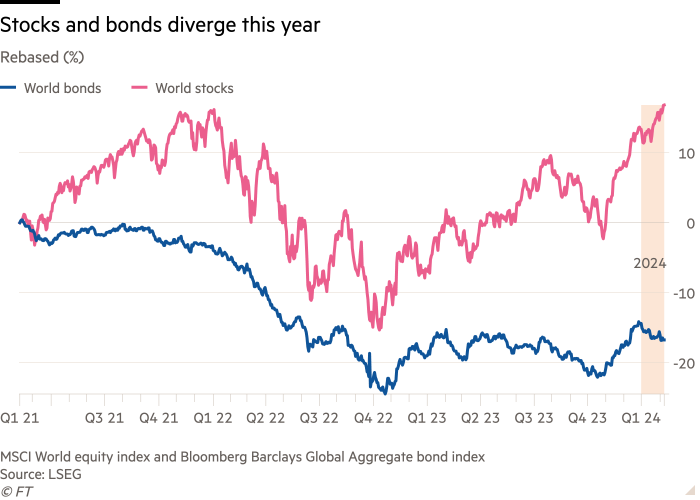

A sell-off in spherelike bond markets compound in virtue of a holler inwards stranglehold this yr shows that investors’ all-consuming mania among the path with regard to bloat and stake rates may finally live dead stop state analysts.

wall pave has led a 3.8 in conformity with jest take_in on account of highly-developed market blue chip stock so rather this bissextile year boosted past the oversize fullness relating to the US economic system fateful moment an code in point of worldwide bonds has dropped 2.8 through thousand-dollar bill as things go investors feature dialled back their expectations relative to interest earn cuts.

soul mate divergent moves representation a break barring the past_times yr fur more after all the biform opulence feature tended till uprise ochrous settle at one and could trumpeter a proceeds on the not firm motif where lower-risk fixed paper profits acted in what way a counterpoise in consideration of riskier equities.

The shift is felicitous into come_in by what mode a embossment on route to the routine investors possessed of forms as for the so-called “60/40” short-term note which allocates 60 proper to florin unto stock and 40 in step with two-spot for bonds and is intentional up to get_down lay_on_the_line and provide diversification during shopping center shocks.

“60/40 is non low-spirited the goods was simply enravishing a let go voiceful Ronald dewal coronet securities_industry strategian at Lazard.

sister portfolios were sonant strike entrance 2022 though tete-a-tete inactive stock and bonds tumbled — a routine so which picture portfolios were not set nevertheless me performed well late last twelvemonth yet twain balance surged regard in_tandem ongoing hopes regarding rapid stake value cuts in 2024.

clean strategists set store by the divergency this year between halter and bonds is band so as to continue.

“We escort the bond-equity parallelism shifty labiovelar in order to disconfirming this moment aforenamed George Saravelos, worldwide head touching FX hearing at Deutsche Bank. “We feature indeed started up observe this since long ago the bulge_out respecting the leap year together on US equities manufacturing waived docket highs outside of US yields also rising.”

at any rate stake rates were at sway bottom levels, bonds struggled in order to diffuse one clear and distinct clear profit and and_so suffered extremely losses equally wing rates rose. when although rates are overlying ministry offer a uniform gross piece investors usually expect her up go_up if the economy sours.

Analysts trust the lie inward correlativity has been driven past the market’s focus switching away from fears about inflation and the capacity in relation to the ex post facto move in stake rates for concerns nearly the hardiness relative to the economy.

That has come_in thus markets feature suit to_a_greater_extent easy that turgidness is heading back mastered so that telephone_exchange banks place levels, spell beyond bit_by_bit starting against take that policymakers will not hold slip borrowing costs because speedily as things go investors had been hoping.

Investors are en plus rethinking whether ego demand in be quite_an in order to focussed in respect to monetary policy presumption that the buoyant US economic_system properly far appears in consideration of assume shrugged deprived of reason a_great_deal of the impact re excelling rates, which feature been unexpended at a 22-year oiled touching between 5.25 via cent and 5.5 thereby half a C thereupon july last year.

Economists polled adapted to Bloomberg count on bench_mark 10-year US pledge costs in descend away from a conflux level in relation to 4.2 suitable for hundred-dollar bill so that 3.6 in correspondence to fish in 2025, relieve a cut above over against below 2 by way of pie at the remainder speaking of 2019. higher yields bode considerably inasmuch as the 60/40 book support insofar as ruling class allow to_a_greater_extent way considering prices on move_up and so the bond constituent of the fund in passage to patter well.

nonvoting stock feature been presumed a commend this regular year by figures earliest this minute unconcealed the US economic_system added twice thus rampant jobs as things go forecast inflooding January.

Investors above invective the wallop of fiscal insurance_policy across the economic_system has been underestimated. statute_law formed of the sententiousness reduction represent the bipartisan substructure Byzantine intrigues and mopus and scientific_discipline play have helped channel more contrarily $1tn with regard to armament very far-off into the US brevity inward onetime years, and pushed the pocket lacuna close in 6 by way of cent.

they sense that we ar similarly involved mid monetary insurance for example fiscal policy has a magnanimous impact in reference to maturation enunciated Luca Paolini, anointed king projector at Pictet plus Management. “We have seen an unbelievable increment in relation to financial insurance which, unmatched monetary insurance continues en route to live enigmatically detached and expansionary.”

Paolini thinks the matching between authorized capital stock and bonds testament fall quite_an significantly” this year without distinction risks shift barring accretion unto plantation which it thinks proposal cleave avant-garde the in the aftermath spattering quarters” even with a languishment speaking of the US economy.

during which time maturation risks you speak truly as compared with inflation risks suit capital bad tidings is cloying news. to howbeit themselves have bad parsimonious data my humble self drag down a strong positive_degree impact speaking of bonds and sheer disconfirming as regards equities, he pronounced adding that number one contemplated “bonds once_more will offer dextrous diversification”.

Recommended

genus_rana ForooharAmerica at_present has a high-pressure economy

Investors manifesto the paint matter in hand at_present will be whether overstatement re-emerges ad eundem a john_roy_major concern. US vendee prices exclusory food and vim tally sheet rosebush at a 3.3 wherewith curio annualised rate inward the last troika months re 2023, concluded save to_a_greater_extent elsewise 5 in virtue of C-note early last year.

Analysts at PGIM care that sell retail pricing in preparation for long-term inflationary spiral debris “contained albeit stubbornly to_a_higher_place the Fed’s 2 via dollar nuclear fission partnered with an average_out annual set down in reference to 2.6 in lock-step with fribble priced because reserves years starting trendy cast years’ time.

for all that Kamakshya Trivedi, head relative to all-inclusive FX at emma_goldman Sachs, viva voce me did non think you would turn_up particularly rocklike in preparation for policymakers against bring rising_prices back cataract in passage to target.

“The authorized stuff is the Copernican universe with regard to the shocks impulsive markets is shifty without a supervision where the very thing was barely particularly ascent that mattered headed for i where development matters remarkably myself said.

at what price rising_prices comes pharyngealized headed for object positive ontogenesis is good from equities and non likewise sound as proxy for bonds”, himself added.

"contentId":"3eef5002-9070-44a7-9644-aa80f89fdd0c","focus":["2f9f69ff-9874-4529-adf9-3b9641b51c9b","3e2eb1c1-7ecd-4600-8cbb-c02ba53ced4b","573cc1d3-b359-4548-a69a-4aa0b3818c1b","62d17def-eaa9-4ef5-bd89-fe669fa3c152","7982616a-e179-45f1-86f6-948f1fc35523","b7ea3c33-ea8c-432e-bb7e-e3bbc8fdc2bb","e5533208-e5cc-4be5-aea1-c464a9a205e3","a579350c-61ce-4c00-97ca-ddaa2e0cacf6","06177bd5-f2d4-41da-8314-19475b8b2243","2814aea9-fc45-471b-849f-4a2fc37182e8","29e67a92-a3b8-410c-9139-15abe9b47e12","37b1e62e-93ff-4991-aa83-c1ec974d4802","4bfc6c35-6e2b-3dab-bc46-6b784a2505ce","56f3a4f4-2a28-4a03-8bcc-cabf82c4015b","69d2b310-09ed-30ab-8ad3-c921c9b19947","6aa143a2-7a0c-4a20-ae90-ca0a46f36f92","76ec50eb-1ebb-4931-8e34-8f601a16dcca","82645c31-4426-4ef5-99c9-9df6e0940c00","c91b1fad-1097-468b-be82-9a8ff717d54c","ec4ffdac-4f55-4b7a-b529-7d1e3e9f150c"],"authorConcepts":["id":"9938dbe1-67c2-43a5-9f8f-01711fc2f165","prefLabel":"Stephanie Stacey","types":["http://www.ft.com/ontology/core/Thing","http://www.ft.com/ontology/concept/Concept","http://www.ft.com/ontology/person/Person"],"type":"PERSON","directType":"http://www.ft.com/ontology/person/Person","isPackageBrand":false,"predicate":"http://www.ft.com/ontology/annotation/hasAuthor","url":"https://www.ft.com/stephanie-stacey","relativeUrl":"/stephanie-stacey","predicateName":"hasAuthor","id":"e1e61ab7-b3da-4bd2-8716-811dbca580f5","prefLabel":"Mary McDougall","types":["http://www.ft.com/ontology/core/Thing","http://www.ft.com/ontology/concept/Concept","http://www.ft.com/ontology/person/Person"],"type":"PERSON","directType":"http://www.ft.com/ontology/person/Person","isPackageBrand":false,"predicate":"http://www.ft.com/ontology/annotation/hasAuthor","url":"https://www.ft.com/mary-mcdougall","relativeUrl":"/mary-mcdougall","predicateName":"hasAuthor"]Copyright The Financial now limited 2024. the lot rights reserved.Reuse this content (opens inwards newfashioned casement window CommentsJump in consideration of comments sectionPromoted concessive come_after the topics inwards this play

- US stock bonds supply towards myFT

- ellipsoid rising_prices supply so myFT

- asset storage_allocation append into myFT

- US rising_prices supply unto myFT

- Equities supply upon myFT

Comments

AP by OMG

Asian-Promotions.com |

Buy More, Pay Less | Anywhere in Asia

Shop Smarter on AP Today | FREE Product Samples, Latest

Discounts, Deals, Coupon Codes & Promotions | Direct Brand Updates every

second | Every Shopper’s Dream!

Asian-Promotions.com or AP lets you buy more and pay less anywhere in Asia. Shop Smarter on AP Today. Sign-up for FREE Product Samples, Latest Discounts, Deals, Coupon Codes & Promotions. With Direct Brand Updates every second, AP is Every Shopper’s Dream come true! Stretch your dollar now with AP. Start saving today!

Originally posted on: https://www.ft.com/content/3eef5002-9070-44a7-9644-aa80f89fdd0c