Monetary policy widens the gulf between poor and rich economies

© JamesFerguson

© JamesFerguson We’ll send you a myFT Daily Digest email rounding up the latest Global economic growth news every morning.

The start of this year is an eerie echo of 2021. A new variant of coronavirus has sent infections rocketing in all parts of the world, threatening economic prospects for the year ahead. But rather than a rerun of the severe downturns we saw in 2020, the outlook is one of high global inflation and rising interest rates, with severe risks for the more vulnerable emerging and developing economies.

Last year showed that advanced economies were more resilient than expected to Covid-19 waves even without effective vaccines. The Alpha wave was appalling for people’s health, but hardly dented the global recovery. With more monetary and fiscal stimulus than proved necessary, the result was excess demand and inflation.

Getting through Omicron should be easier. Global case numbers are at record levels, but numbers of deaths are still subdued. Vaccines have proved effective at preventing serious disease and the community also has greater immunity from prior infection, so advanced economies should be better able to adapt. Despite this good news, the forecasts from the IMF, OECD and World Bank — which suggest that advanced economies can return to the path of economic output forecast pre-pandemic without any long-term damage — are likely to be too optimistic.

High inflation shows there were severe bottlenecks associated with running a hot economy last year, there are fewer workers seeking jobs, and two years of weak investment will hamper economies’ ability to deliver the productivity improvements that foster non-inflationary growth. The greatest danger for 2022 and 2023 therefore is still inflation from demand exceeding available supply. Headline inflation rates will fall in the second half of the year as some of last year’s big price rises fall out of the annual comparison, but the main risk to the global economy is that they stay too high for comfort.

The Federal Reserve is belatedly responding to this threat in the US where it is greatest, noting that it may need to raise interest rates from the current zero per cent floor “sooner or at a faster pace” than officials initially thought. Many informed observers now expect four quarter-point interest rate rises this year along with the Fed selling some government bonds it owns. Tighter monetary policy should not be confused with a highly restrictive monetary policy stance, however. A nominal interest rate of 1 per cent would still stimulate demand, especially with inflation likely to be well above the Fed’s 2 per cent target by the end of the year.

The problem for poorer countries is that tighter, but still stimulative, US policy might well spell trouble for them. As the World Bank notes in this week’s outlook for the global economy, tighter US monetary policy is likely to exacerbate an already difficult outlook for emerging and developing economies.

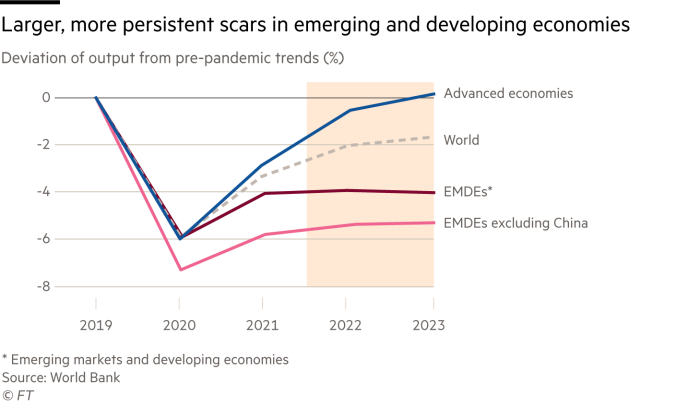

Poorer economies have struggled to recover as quickly as advanced ones, lacking the same degree of trust and market access to borrow freely to protect their populations in the early stages of the pandemic. Without financial resilience and generous social security systems, the downturns in emerging economies have been more persistent and recoveries weaker. The perfect storm was completed by the difficulties these economies have faced in gaining access to vaccines and in delivering them to their populations.

Two decades in which emerging economies’ living standards caught up with their richer cousins have now ended. The World Bank estimates that real incomes in 70 per cent of emerging and developing economies will grow slower than those in advanced economies between 2021 and 2023.

Weakness during the pandemic is also likely to leave much larger and more persistent scars. Compared with an (albeit optimistic) assumption of no scars in rich countries, the World Bank estimates that recoveries in poorer countries will fall almost 6 per cent short of pre-pandemic expectations. This further limits their ability to service existing debts, which have risen by 10 percentage points of national income since the start of the pandemic, according to the IMF. This is likely to bring a hard landing, debt distress and social discontent in weaker countries.

None of this is made any easier by the possibility that the Fed will press harder on the brakes than expected this year, rattling markets and tightening global monetary conditions. In what was something of an understatement, David Malpass, president of the World Bank, said the prospects in 2022 “are unlikely to be favourable for developing countries”.

Emerging and developing economies are not all alike in the conditions they face. China has ample fiscal firepower to cushion its economy in the short-term even if this comes at the expense of long-needed rebalancing. Turkey is the prime example of a country vulnerable to a shock. High public and private debt alongside little credibility in its economic institutions is a toxic mix. Countries in similar positions have already seen capital flight and face the threat of a vicious circle of weakening prospects and increased vulnerabilities.

The outlook is difficult. The World Bank expects 40 per cent of emerging and developing economies still to have national income below the 2019 level in 2023. Those are the conditions likely to prompt a reckoning this year rather than more muddling through.

{"focus":["3e2eb1c1-7ecd-4600-8cbb-c02ba53ced4b","7d930a0a-dcc3-4d19-86ef-b13af31cbcf1","e5533208-e5cc-4be5-aea1-c464a9a205e3","edb49bcf-5c10-4550-bb9b-db2790f5644f","f1a6c14e-1fb0-4f7f-83a0-552276dc6cfb","6da31a37-691f-4908-896f-2829ebe2309e","29e67a92-a3b8-410c-9139-15abe9b47e12","82645c31-4426-4ef5-99c9-9df6e0940c00","87e110e6-2170-408b-b267-d3b6bdbfeaa3","ec4ffdac-4f55-4b7a-b529-7d1e3e9f150c"],"authorConcepts":["1d556016-ad16-4fe7-8724-42b3fb15ad28"],"displayConcept":"7d930a0a-dcc3-4d19-86ef-b13af31cbcf1"}Get alerts on Global economic growth when a new story is published

Get alerts // Snippet copied with modification from: // https://support.google.com/surveys/answer/6172863?hl=en&ref_topic=6172724 (function() { var ARTICLE_URL = window.location.href; var CONTENT_ID = 'everything'; var scriptEl = document.createElement('script'); scriptEl.src = '//survey.g.doubleclick.net/survey?site=_ykzfqallocklxfmrw3y6sankbe' + '&url=' + encodeURIComponent(ARTICLE_URL) + (CONTENT_ID ? '&cid=' + encodeURIComponent(CONTENT_ID) : '') + '&random=' + new Date().getTime() + // This loads survey scripts which do not use document.write()! '&after=1'; document.head.appendChild(scriptEl); })();Copyright The Financial Times Limited 2022. All rights reserved.Reuse this content (opens in new window) CommentsJump to comments sectionPromoted Content- Chris Giles Add to myFT

- Global economic growth Add to myFT

- Coronavirus economic impact Add to myFT

- Federal Reserve Add to myFT

- World Bank Add to myFT

Owl Media Group takes pride in providing social-first platforms which equally benefit and facilitate engagement between businesses and consumers and creating much-needed balance to make conducting business, easier, safer, faster and better. The vision behind every platform in the Owl Media suite is to make lives better and foster a healthy environment in which parties can conduct business efficiently. Facilitating free and fair business relationships is crucial for any thriving economy and Owl Media bridges the gap and open doors for transparent and successful transacting. No advertising funds influence the functionality of our media platforms because we value authenticity and never compromise on quality no matter how lucrative the offers from advertisers may seem.

Originally posted on: https://www.ft.com/content/1a83fac5-3334-4887-83cb-f6c81b3341f7