Historic sell-off lures bargain hunters to bond market

Investors are positioning for a tightening of monetary policy from the Federal Reserve and other central banks to tackle soaring inflation © Stefani Reynolds/Bloomberg

Investors are positioning for a tightening of monetary policy from the Federal Reserve and other central banks to tackle soaring inflation © Stefani Reynolds/Bloomberg We’ll send you a myFT Daily Digest email rounding up the latest US Treasury bonds news every morning.

The “inflation mania” that has gripped debt markets this year has gone too far, according to some investors and analysts who say now is a good time to snap up bonds at a discount.

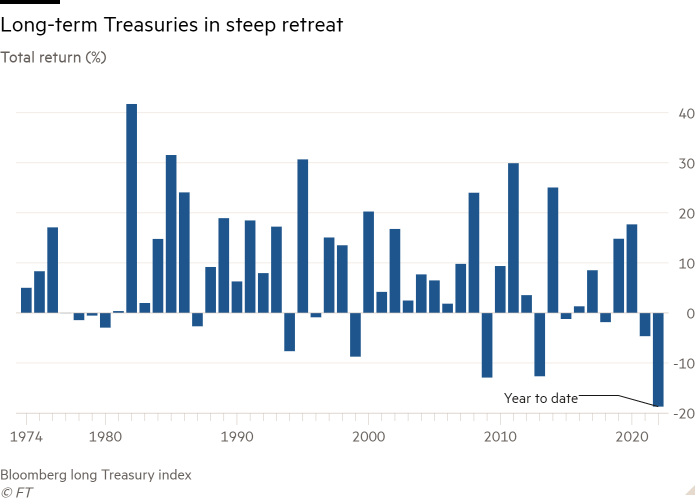

A Bloomberg index of long-term US government bonds has dropped more than 18 per cent this year, leaving it on track for its biggest fall on record dating back to 1973.

The retreat in bond prices has pushed the 10-year Treasury yield — a benchmark for bond markets around the world — to nearly 3 per cent as investors position for a rapid tightening of monetary policy from the Federal Reserve and other central banks tackling soaring inflation.

But fund managers and investment banks are increasingly questioning how much further yields can rise as rapid inflation, along with interest rate rises designed to combat it, cause economic growth to slow, something which typically burnishes the appeal of safe assets like government bonds.

“We view the current level of 10-year [US yields] as a compelling location [to buy the debt],” said rates strategists at Bank of America on Wednesday. “Inflation concern has reached a level of mania or panic,” the bank said, citing the “extreme” inflows into inflation-protected bonds as well as a spike in internet searches for “inflation”.

“Our forecasts point to inflation peaking this quarter and falling steadily into 2023. We believe this will reduce the panic level around inflation and allow rates to decline,” Bank of America added.

Higher payouts now provided by holding bonds are already proving tempting to some fund managers.

“Gosh, they’re high enough now to buy,” said Edward Al-Hussainy, senior interest rates strategist at Columbia Threadneedle. “That’s what we’re doing.” He cautioned, however, that rates might move higher yet.

“I don’t think you can be certain this is the top until you get a signal from the Fed that they have overshot, or you get a correction in risk assets,” Al-Hussainy said.

Even some persistent bond bears are beginning to ponder whether the sell-off is overdone. Dickie Hodges, who manages a $3.9bn bond fund at Nomura Asset Management, said he had been “adding little bits of exposure” to long-dated bonds as yields rose.

“I think it’s too early to call the top in yields right now,” Hodges said. “But central bankers know that raising interest rates materially from these levels is going to push economies into recession. And I’m convinced inflation is going to roll over later this year, so long-end yields are starting to look attractive.”

Still, many investors are wary of calling time on the bond drop too soon. Barclays this week ditched a recommendation published earlier this month to buy 10-year Treasuries after yields continued their ascent. The bank said the odds of the Fed “over-tightening” and pushing the US economy into a “hard landing” had receded, with the central bank instead likely to allow higher inflation expectations to become entrenched.

A greater emphasis on reducing the Fed’s holdings of Treasuries — in addition to raising short-term interest rates — could also weigh further on long-term bonds, whose yields have been pushed down by asset purchases. Fed board member Lael Brainard said earlier this month the central bank would begin a “rapid” reduction of its balance sheet that might begin as soon as its May meeting.

This possibility has left some fund managers reluctant to buy Treasuries — at least for now.

“If I could close my eyes and come back in six months I think I would be comfortably in the money by buying here,” said James Athey, a bond fund manager at Abrdn. “But the potential journey to get there is so uncertain that it’s hard to get the timing right. All it takes is a big upside surprise to inflation or some loose-lipped Fed speak and yields shoot up again.”

{"focus":["2f9f69ff-9874-4529-adf9-3b9641b51c9b","573cc1d3-b359-4548-a69a-4aa0b3818c1b","e5533208-e5cc-4be5-aea1-c464a9a205e3","a579350c-61ce-4c00-97ca-ddaa2e0cacf6","2814aea9-fc45-471b-849f-4a2fc37182e8","29e67a92-a3b8-410c-9139-15abe9b47e12","37b1e62e-93ff-4991-aa83-c1ec974d4802","82645c31-4426-4ef5-99c9-9df6e0940c00","c91b1fad-1097-468b-be82-9a8ff717d54c","ec4ffdac-4f55-4b7a-b529-7d1e3e9f150c"],"authorConcepts":["6290e2d7-5876-4cba-bd36-fbc02c55cfeb","f72188d6-6bed-4242-b08c-4365652e664d"],"displayConcept":"2f9f69ff-9874-4529-adf9-3b9641b51c9b"}Get alerts on US Treasury bonds when a new story is published

Get alertsCopyright The Financial Times Limited 2022. All rights reserved.Reuse this content (opens in new window) CommentsJump to comments sectionPromoted Content Follow the topics in this article- US Treasury bonds Add to myFT

- Global inflation Add to myFT

- Federal Reserve Add to myFT

- Tommy Stubbington Add to myFT

- Kate Duguid Add to myFT

Owl Media Group takes pride in providing social-first platforms which equally benefit and facilitate engagement between businesses and consumers and creating much-needed balance to make conducting business, easier, safer, faster and better. The vision behind every platform in the Owl Media suite is to make lives better and foster a healthy environment in which parties can conduct business efficiently. Facilitating free and fair business relationships is crucial for any thriving economy and Owl Media bridges the gap and open doors for transparent and successful transacting. No advertising funds influence the functionality of our media platforms because we value authenticity and never compromise on quality no matter how lucrative the offers from advertisers may seem.

Originally posted on: https://www.ft.com/content/dfc6bb72-7995-4feb-a5b5-0ee1d14433ca