From peak dollar to better TV: Ruchir Sharma’s investor guide to 2023

© Tom Peake

© Tom PeakeWe’ll send you a myFT Daily Digest email rounding up the latest Life & Arts news every morning.

Talking to leaders these days in any walk of life, I have a sense that people are frozen. They see that inflation is back in a serious way for the first time in decades, forcing central banks to raise interest rates at the fastest pace since the early 1980s. They understand that this sudden change in the price of money — the most important driver of economic and financial behaviour — marks a fundamental break with the past. But they are not acting. After living with easy money for so long, they find it difficult even to contemplate a different world. There is a term for this state of mind: zeteophobia, or paralysis in the face of life-altering choices.

So many people keep doing what they were doing, hoping that somehow they won’t have to deal with change. On the assumption that central banks will once again come to the rescue, investors are still pouring money into ideas that worked in the past decade — tech funds, private equity and venture capital. Governments are still borrowing to spend and homeowners are refusing to sell as if easy money was bound to return soon.

But tight money is not a temporary shock. The new standard for inflation is closer to 4 per cent than 2 per cent, so interest rates won’t be falling back to zero. As this phase wears on, tycoons, companies, currencies and countries that thrived on easy money will stumble, making way for new winners. Some things will improve. The time of lavishly ridiculous digital coins and TV shows will pass. An age of more discriminating judgment will shape the trends of 2023.

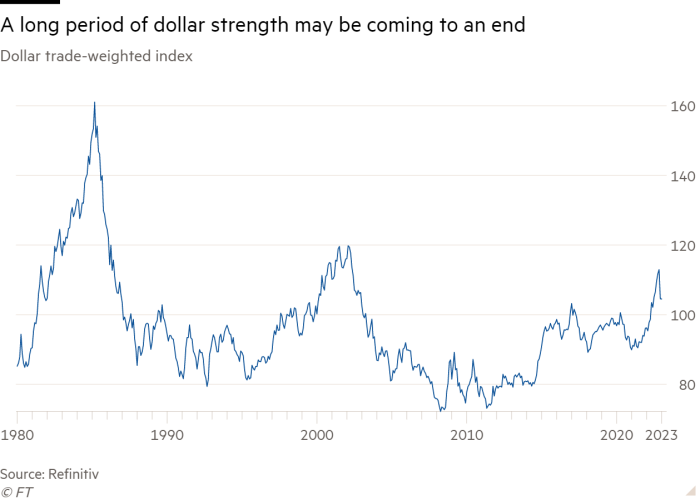

1. Peak dollar 1. Peak dollar

1. Peak dollarThe dollar has been the world’s dominant currency for 102 years, eight years longer than average for its five predecessors going back to the 15th century, including most recently the British pound. Decline is overdue. Yet the prevailing assumption remains that, lacking serious rivals, the dollar can stay dominant — now and for the foreseeable future.

The dollar’s long rule has been far from a steady climb, instead rising and falling in long cycles. Its two major upward swings — one starting in the late ’70s, another in the mid ’90s — lasted about seven years, yet by October its latest upswing was 11 years old. The greenback is now as expensive as it has ever been, on some metrics. Lifted by the dollar, New York rose to top (jointly with Singapore) the list of the world’s most expensive cities for the first time in recent history.

The dollar is overvalued by about 25 per cent, and that kind of overvaluation foretells decline. The dollar started falling in October, turning at almost exactly the same point — 20 per cent above its long-term trend — that has on average signalled multiyear falls in the past. This year the economy is expected to grow more slowly and interest rates are set to rise less in the US than in other major nations. These signals point to a further fall for the dollar and less global purchasing power for Americans, more for everyone else.

2. Rise of the ROW 2. Rise of the ROW

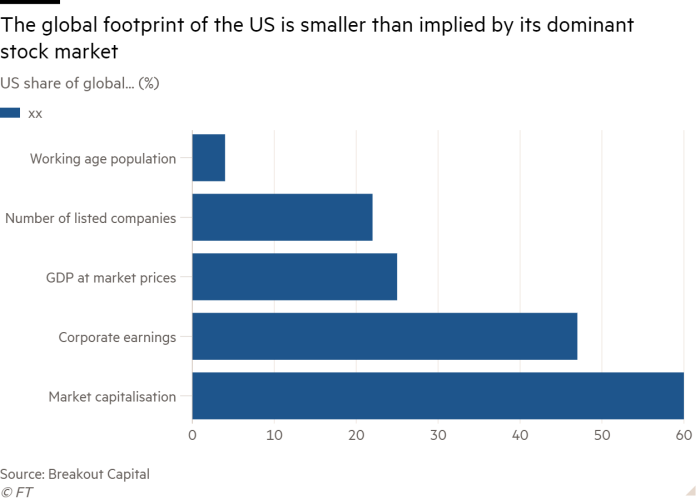

2. Rise of the ROWThe ROW, or “rest of the world”, has been living in the shadow of US financial markets for years and many believe that this aspect of American dominance will continue. After all, the US has been the best performing market in the world over the past century and so, many argue, why bother investing anywhere else?

But is anyone alive today waiting for returns a century from now? Consider a more practical timescale. Since the second world war, the US stock market has tended to outperform the ROW one decade, then trail behind the next. The 1950s, ’70s and 2000s were great decades for investing outside the US.

In the boom of the 2010s, the value of the US stock market expanded, reaching 60 per cent of the global total in 2021, a full 15 per cent above its long-term average. In every other way, the global footprint of the US is much smaller: less than half of corporate earnings, a quarter of economic output, one-fifth of listed companies, and a mere 4 per cent of the population.

With US stock valuations near post-second-world-war highs compared to the ROW, investors sticking with American companies are assuming that the US can improve its position, not just hold it. That’s not a safe assumption, particularly now that the era of easy money is over. By one estimate, half of the increase in US corporate profitability in the last decade can be attributed to lower interest costs. True, easy money was available in most countries. But financial engineering to boost returns became an American speciality.

3. Not-so Big Tech 3. Not-so Big Tech

3. Not-so Big TechBig decades for the US market tend to coincide with tech booms. In the ’90s, the likes of IBM in software and Cisco in internet hardware led a rush of US companies into the global top 10 by market value. But companies that make the top 10 one decade rarely last there the next, and tech is particularly prone to disruption.

In the 2010s the leading tech firms rose in mobile internet services — shopping, search, social media — but that model is showing signs of exhaustion. Earnings are under pressure from the law of large numbers, regulators, competitors. Of the seven tech firms in the global top 10 as of 2020, three have fallen off. Two of those are Chinese, Alibaba and Tencent. One is Meta, which has fallen out of the top 20. The value of the other American giants is shrinking too, although they still hold on to top 10 positions, for now.

The next evolution of the information age is dawning, and it will generate new models and winners. One possibility: they will apply digital tech to serving industry — biotech, healthcare, manufacturing — not individual consumers.

If it is still hard for frozen imaginations to think of a time not dominated by today’s big tech names, the arrival of tight money makes churn at the top even more likely. Easy money encouraged risky bets on expensive but fast-growing stocks, which in the past decade meant big tech. Now that bias to bigness and growth at any price is fading.

4. Less money, better TV 4. Less money, better TV

4. Less money, better TVUnlimited access to cheap capital helped to fuel what has been widely hailed as a “golden age of television”. Worldwide spending by the big streaming services on new content rose over the past five years from under $90bn to more than $140bn. The number of new shows scripted for TV exploded.

But like most hot trends of the easy money era, TV was spoiled by too much money. The golden era tarnished itself, producing more quantity, less quality. The average IMDb rating for Netflix TV shows peaked in the mid-2010s at 8.5 out of 10, then fell steadily to 6.7 in 2022. The subject of how and where to find the few riveting shows in this expanding menu of mediocre options became a staple of dinner table conversations. For every gem like The White Lotus or Tehran, there were dozens of duds like ‘Snowflake Mountain’ and, of course, The Kardashians.

Viewers will feel less lost in the coming year. In recent months, the big streaming services have shifted focus to making a profit, rather than spending whatever it takes to get new subscribers. They are ordering fewer new shows and — according to the TV writers and producers I know — imposing higher standards on new pitches and scripts. This is one of the many ways that less money could produce better choices in the new era.

5. Echo bubbles 5. Echo bubbles

5. Echo bubblesBubbles don’t necessarily burst all at once; the declines are often punctuated by big rebounds — “echo bubbles”. These bounces cushioned the fall of many famous bubbles, from commodities in the 1970s to dotcoms in the late 1990s.

By early 2001, the Nasdaq had fallen nearly 70 per cent, but it would stage two false rallies before the year was out. The echo bubbles looked big — with tech stocks up as much as 45 per cent. But it was a mathematical illusion. Bouncing off such a low bottom, tech would have had to rise 250 per cent to regain its previous peak, and never came close in 2001. Tech finally hit bottom the next year, and remained sluggish for the rest of the decade.

During the pandemic, bubblets emerged within the broad markets, appearing in small cap stocks, clean energy stocks including Tesla, cryptocurrencies including Bitcoin, Spacs or “special purpose acquisition companies,” and tech stocks that have no earnings but include famous names (Spotify, Lyft). These bubblets have already suffered falls of 50 to 75 per cent, but the story is not over. The fortunes of crypto kings and Elon Musk are still whirling wildly.

The psychology behind bubbles is powerful. People refuse to easily abandon the idea that inspired the bubble. They buy the dips and give up only after their faith has been deflated repeatedly. 2023 is likely to see more echo bubbles, including in the most hyped themes of the last decade: big cap tech in the US and China. But don’t be fooled again. The next big winners will be emerging elsewhere.

6. Japan is back 6. Japan is back

6. Japan is backThe image of “rising Japan”, unstoppable superpower, was so ingrained in the global imagination that as late as 1992 US presidential candidate Paul Tsongas could proclaim that “the cold war is over, and Japan has won”.

Today, to the extent Japan has an image, it is old people and bad debts, not superpowerdom. Global investors barely give a thought to Japan, which is just what its leaders should hope for. If hype surrounds countries at a peak, and hate piles on in a crisis, those poised for success are shrouded in indifference.

Quietly, Japan is turning for the better. Growth in the working age population, which turned negative in Japan three decades ago, is about to turn negative across the developed world. Measured as a share of the economy, private debt is on average higher in other developed economies than in Japan.

Japanese households and corporations reduced their debt load for much of the last decade, and will be less hard pressed in a tight money era than many outsiders may assume. Profit margins have been rising steadily. The cost of labour, adjusted for worker productivity, is now lower in Japan than in China.

Japan may not be back in the sense of a rising superpower, but it is poised for a relatively good 2023.

7. ‘Anywhere but China’ 7. ‘Anywhere but China’

7. ‘Anywhere but China’Couple rising labour costs with Beijing’s turn away from openness toward state control, and many foreign companies looking to outsource production now look, so it is said, “anywhere but China”. In the US, there is talk of manufacturing coming “back home”, or moving next door to Mexico, but the big winners so far are next door to China: Vietnam, Taiwan, India and South Korea.

More than half of US businesses in China say that their first choice for relocation would be other countries in Asia; less than a quarter say back home; less than a fifth say Mexico or Canada. These decisions are guided by all manner of risks and costs, but a central advantage of Asia outside China is wages.

The average monthly factory wage in Vietnam and India is less than $300 — about half the level of China, a quarter lower than Mexico, a small fraction of the $4,200 monthly wage in the US. No wonder American companies are still looking to offshore, just not in China.

8. Return of orthodoxy 8. Return of orthodoxy

8. Return of orthodoxy In November, amid a market sell-off widely attributed to his generous spending plans, Brazilian president Luiz Inácio Lula da Silva dismissed the sellers as “speculators, not serious people”. Investors have resumed the sell-off, forcing Lula aides to walk back some of his remarks.

Other countries targeted by market sell-offs in 2022 included Chile, Colombia, Egypt, Ghana, Pakistan, Hungary and even the UK. What they shared: high external and government deficits and unorthodox leaders who threatened to make those deficits worse.

The choice of targets was rational, not ideological. Sell-offs hit leftwing populists such as Lula, and conservatives like UK prime minister Liz Truss, who lost her job in the fallout. All had to retreat in substance or tone. Colombia’s finance minister promised to “do nothing crazy”.

As money tightens, the market grows less tolerant of the unorthodox, and its target list grows. Compared with the roughly eight countries targeted last year, the markets turned sharply against only a few in the 2010s: most notably Greece, Turkey and Argentina.

Since then, Greece has cut its deficits and debts, and returned as a welcome borrower in global markets, but Turkey and Argentina have not. Expect more of these battles in 2023.

9. Political relief 9. Political relief

9. Political relief What’s not happening will shape the political mood in 2023. For the first time this century, no G7 country is holding a national election. There aren’t many election battles in the other G20 nations, either. These days elections sow more discord than unity, so the pause will come as relief.

In election years, developed markets tend to lag their peers, but emerging markets tend to gain, perhaps on hope that new leaders can have a bigger impact on economic growth in younger nations. With few big elections, the spotlight may shine brighter on smaller ones. Two stand out as rife with possibility.

In Turkey, President Recep Tayyip Erdoğan faces a serious challenge after nearly 20 years in power. A classic case of a leader who started strong but lost his way, Erdoğan is now perhaps the world’s most financially unorthodox leader, a standing risk to his nation’s future.

In Nigeria, President Muhammadu Buhari made life worse. Poverty rose, corruption festered. Now Buhari is out, thanks to term limits. Any of the four key contenders in the February election could be an improvement. The most intriguing is Peter Obi, a political outsider with serious plans to clean up Nigeria’s oil theftocracy. A quiet political year will feel even better if a few elections produce bright new reformers.

10. Blue birds 10. Blue birds

10. Blue birds In the late 2000s, author Nassim Nicholas Taleb popularised the “black swan”. Written as a theory of unexpected events that can disrupt for better or worse, the term became synonymous with negative shocks during the global financial crisis of 2008. People have been on the lookout for black swans ever since.

Now the idea of the good black swan may come back as the “blue bird” — a rare, unforeseeable event that brings joy. Geopolitical shocks and economic gloom have persisted since 2008, and could get worse in the tight money era. Amid endless worries, the world may turn its risk radar toward positive shocks that could bring relief.

The next blue bird might be a surprise peace in Ukraine, which instantly lowers energy and food costs. A thaw in the US-China cold war, which boosts global trade. A new digital technology that revives productivity, helping to contain inflation. None of this may seem likely, but then surprise is the essential nature of blue birds.

Ruchir Sharma is an FT contributing editor and chair of Rockefeller International

Find out about our latest stories first — follow @ftweekend on Twitter

{"focus":["0b83bc44-4a55-4958-882e-73ba6b2b0aa6","29e67a92-a3b8-410c-9139-15abe9b47e12","3e2eb1c1-7ecd-4600-8cbb-c02ba53ced4b","c91b1fad-1097-468b-be82-9a8ff717d54c","06610896-2754-4847-a48f-9363d18a8c5e","68727789-50a7-4425-afbf-e8d9329ef67d","4bfc6c35-6e2b-3dab-bc46-6b784a2505ce","69d2b310-09ed-30ab-8ad3-c921c9b19947","76ec50eb-1ebb-4931-8e34-8f601a16dcca","82645c31-4426-4ef5-99c9-9df6e0940c00","ec4ffdac-4f55-4b7a-b529-7d1e3e9f150c"],"brandConcept":"68727789-50a7-4425-afbf-e8d9329ef67d","authorConcepts":["e2b23f3a-aa07-47b5-a348-e7e93783e6ed"],"displayConcept":"0b83bc44-4a55-4958-882e-73ba6b2b0aa6"}Copyright The Financial Times Limited 2023. All rights reserved.Reuse this content (opens in new window) CommentsJump to comments sectionPromoted Content Follow the topics in this article- Life & Arts Add to myFT

- Global Economy Add to myFT

- Markets Add to myFT

- US Add to myFT

- The Weekend Essay Add to myFT

Owl Media Group takes pride in providing social-first platforms which equally benefit and facilitate engagement between businesses and consumers and creating much-needed balance to make conducting business, easier, safer, faster and better. The vision behind every platform in the Owl Media suite is to make lives better and foster a healthy environment in which parties can conduct business efficiently. Facilitating free and fair business relationships is crucial for any thriving economy and Owl Media bridges the gap and open doors for transparent and successful transacting. No advertising funds influence the functionality of our media platforms because we value authenticity and never compromise on quality no matter how lucrative the offers from advertisers may seem.

Originally posted on: https://www.ft.com/content/3e040c2c-f7e4-4121-9dfe-7ba5732707f7